Consumer-Commerce Insights | India

What is working in Consumer Commerce, why & How ? || Emerging Spaces & Success Models (No Fluff -2024)

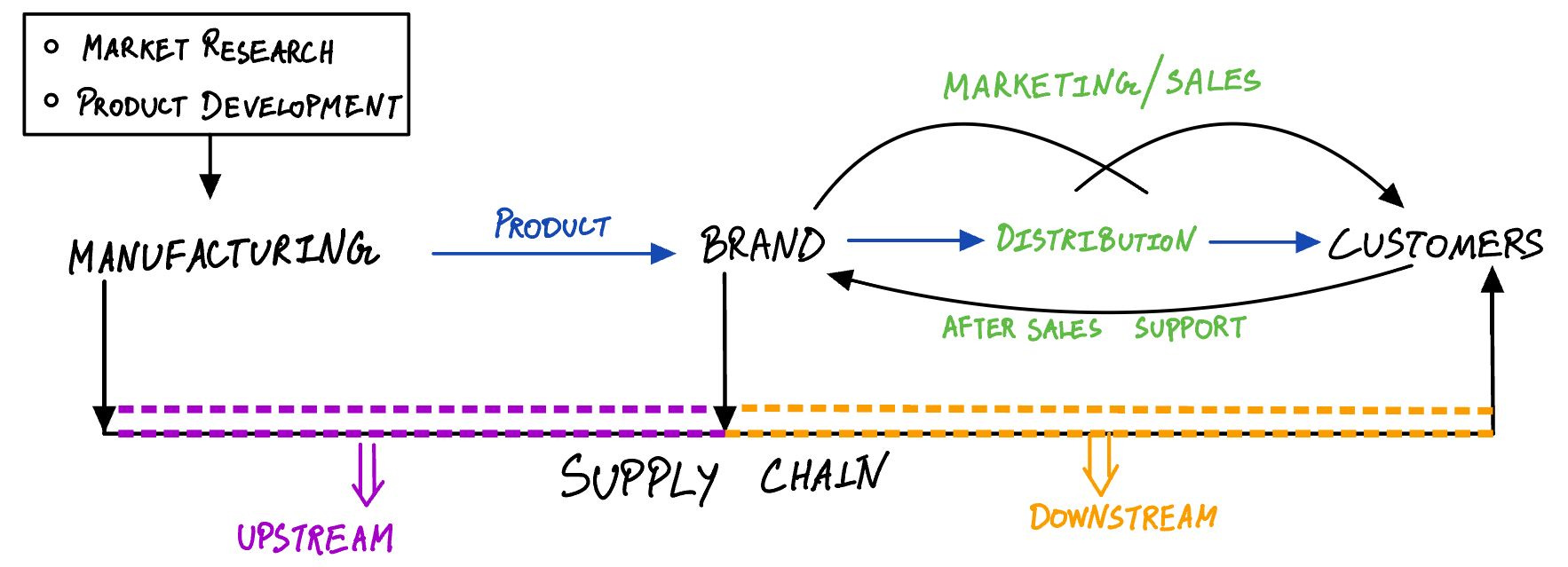

What does commerce look like for a consumer brand :

Downstream :

Distribution

Interesting segments to study :

Looking at Distribution for Consumer Brands

Green - New / Open spaces with early stage models (V 3.0)

Orange - Fairly long existing spaces with few established played (V 2.0)

Red - Long standing Incumbents in these spaces (V 1.0)

Marketing & Sales - ECommerce Enablement

Classified into:

Few Successful companies in Sales: E-comm Enablement:

Insights New Consumer Brands to Grow:

New Consumer brands are witnessing exciting growth, Why ?

Successful Outcomes

Q-Comm Tailwinds

Changing Consumer Behaviour

Successful Outcomes

D2C as a segment had lost interest with most investors from 2019 - 2023 But has been seen a resurgence of interest in the D2C sector, due to:

Success of VC backed consumer brand with successful outcomes:

Mamaearth

First Cry

LensKart

BoAt etc.

REVENUE (high growth)

Q-commerce

Fairly Large / Multiple Opportunities (V 3.0) in Downstream present which are powering new-age commerce :

Around rejuvenation of Retail

Around Quick-Commerce

The Gross Merchandise Value (GMV) of India's quick commerce industry increased to $3.3 billion in the financial year 2023-24, compared to $500 million in the financial year 2021-22, registering a nearly 280% increase, according to the report.

Trend and future outlook

How is the Q-Comm supply chain designed ?

Current Supply Chain for Quick Commerce :

Where are 3PL Q-Comm Enablers comming in ?

Combination of :

Retail Outlet + 3. Last mile

Dark-Store + 3. Last Mile

All combined / hybrid → For better order density

Changing Consumer Behaviour:

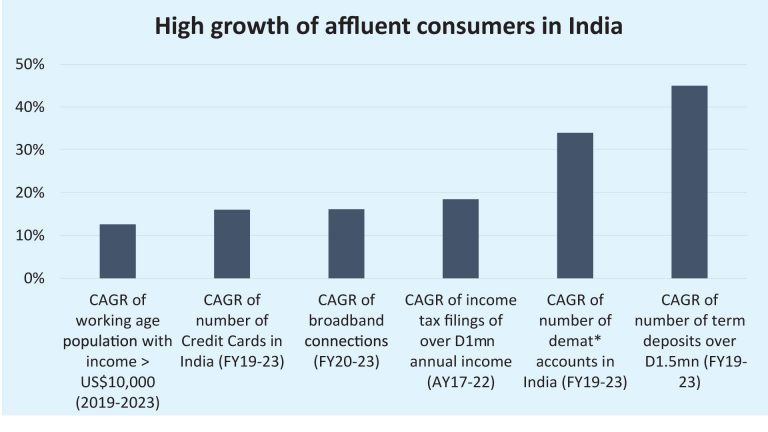

Premiumization

Key Drivers of Premiumization

Rising Affluence: The expansion of India's middle class has resulted in increased disposable incomes, allowing consumers to explore premium offerings beyond basic needs. This demographic shift is particularly evident in Tier 1 and Tier 2 cities, where aspirations for quality products are growing rapidly

Aspirational Shift: Urbanization and exposure to global brands have fostered a desire for better lifestyles among Indian consumers. Premium products are increasingly associated with status and success, leading consumers to invest in higher-quality goods

Digital Influence: The rise of social media and online platforms has heightened consumer awareness and comparison

Evolving Retail Landscape: Modern retail formats, both online and offline, have made premium products more accessible.

Quality Over Price: Today's consumers prioritize quality, durability, and after-sales service over mere affordability.

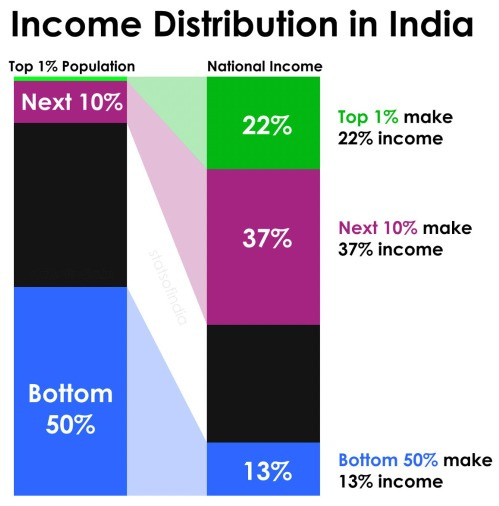

I see it in 3 buckets in Consumers in India :

The Urban affluent

The Tier 2+ mindset

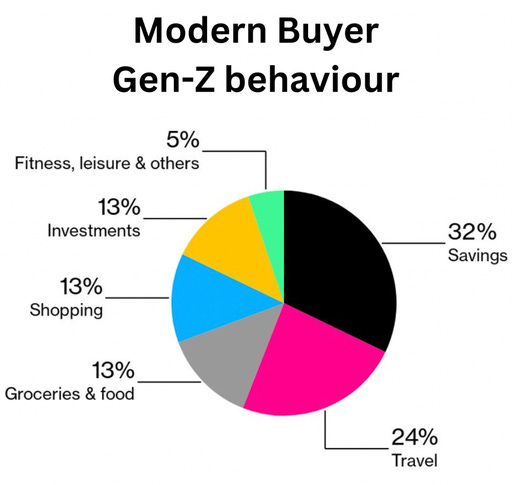

The modern buyer (Gen-Z ++)

A few distinct characteristics for each group :

URBAN AFFLUENT

Usually around 24 - 45 age group

Work and live in Metros (more % salaried, less % self-employed)

Income is mostly > 1 lac / month, with significantly disposable portion

Shops 40%+ online

Aspires to be in the top 1%

Often flaunts through branded products

Wants convenience, travel, premium products (Q-commerce’s & major OTT platform users)

Least fussy about price for good value

TIER 2+ MINDSET

Not age-restricted

Living in either Urban (Boomers or Generation X) or Tier 2+ geography

Income usually > 2 lac / month of the household (less % salaried or more % self-employed)

Shop ~ 10-30% online

Aspires to be locally most successful

Their perception in the community / society matters a lot to them

Seek hyper-value (Think Big Bazaar customers)

Price sensitive - love the discount / bargain deals

MODERN BUYER (GEN-Z ++)

Usually < 25 years (think 1st Job professionals / college students)

Mostly in top 10 cities on India

Just started earning or usually dependent on family for monthly expenses 10K to 1 lac / month

Shop 60+% online (driving ecomm growth in non-metros as KOL in the household)

Aspire to have freedom to do what they want - figuring out their job / business

Stay upto date with fashion trends, social media, think about saving / investing

Seek quality in smaller brands / boutique offerings

Price not a barrier if affordable (on EMIs) with monthly allowances

UPSTREAM:

Contract Manufacturing

Domestic

Cross-border → Think how all major brands have their factories in China

Macros in favour :

Increased Contract Manufacturing and Outsourcing

Interesting sub-sectors :

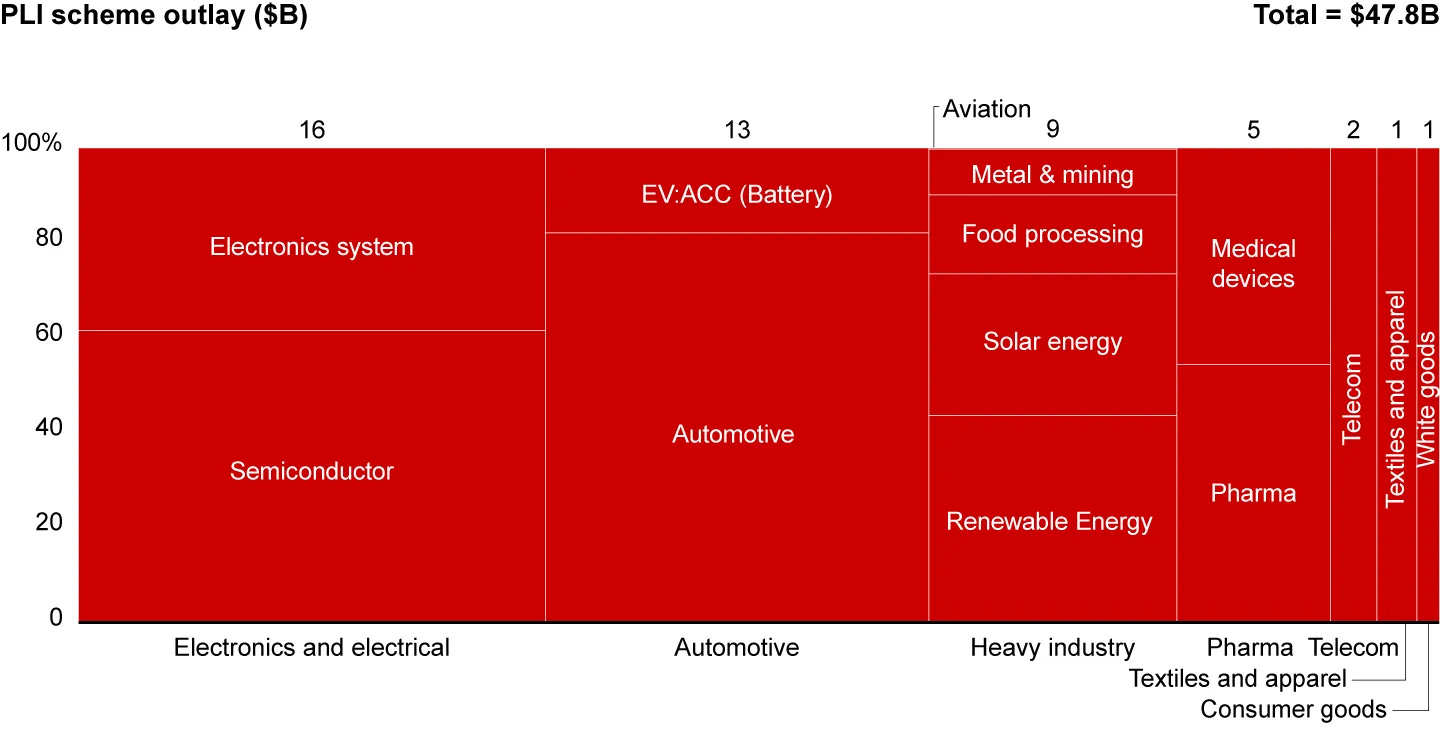

2. Government Policies and Incentives

Make in India and Atmanirbhar Bharat: These initiatives aim to make India a global manufacturing hub, particularly in key sectors like electronics, automotive, and pharmaceuticals.

PLI Schemes: The government has rolled out PLI schemes for several sectors, incentivizing domestic manufacturing and attracting foreign investments in upstream industries.

Favorable Tax and Regulatory Environment: The easing of tax regulations, such as GST reform, and policy support have made India more attractive for international companies seeking contract manufacturing partners.

To conclude there are several Macro + Micro factors and open / emerging spaces in the Indian Consumer Commerce which will eventually be capitalised by startups or incumbents.