HealthCare vis-à-vis Startups | India

Why is the Indian Health industry so difficult to crack || White Spaces & Success Models

Indian Health Care system is much different than the largest health systems we know about :

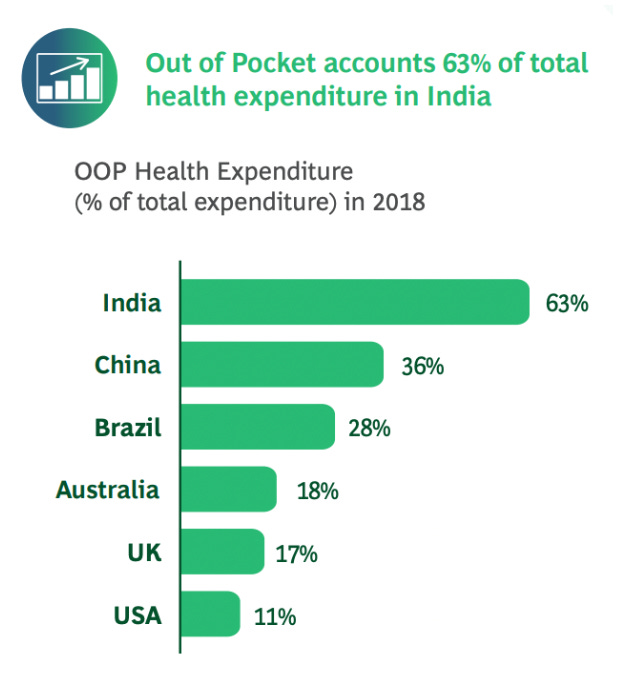

Expenditure: India Health Expenditure per Capita is around $74.00 (source), and hence cannot be compared with developed nations, Indian HealthCare needs disruption

Health Care Expenditure per capita

How do these countries afford such expenses: Insurance

Most developed countries have > 80% people covered under some form of health insurance (private + public)

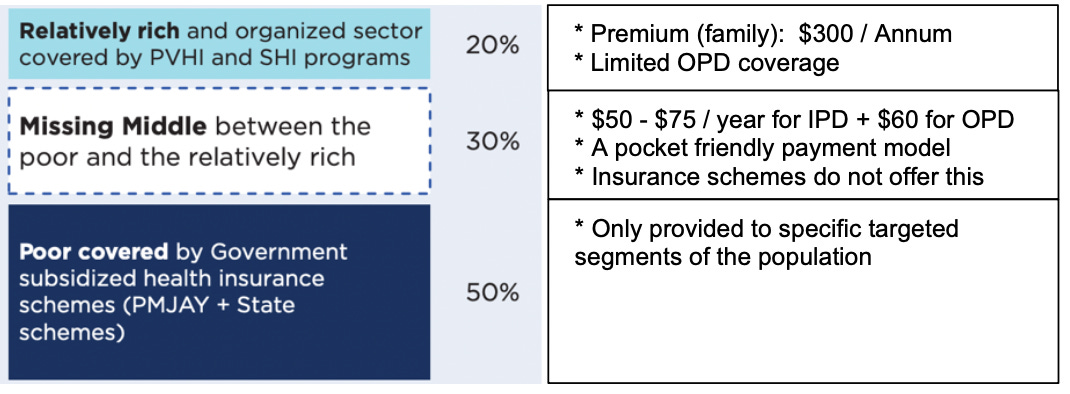

Health Insurance penetration in India

~50% of bottom economic strata is covered under the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB PM-JAY) + state scheme for Secondary & Tertiary Care

~18% Indians have voluntarily opted for Health Insurance

~ 30% of middle class has no-coverage at all

Leading to → High out of pocket expenses for individuals

India needs disruptors to solve for Indian health care industry.

Paths for Health Care startups in India :

A) Creating disruption in Health Insurance in India

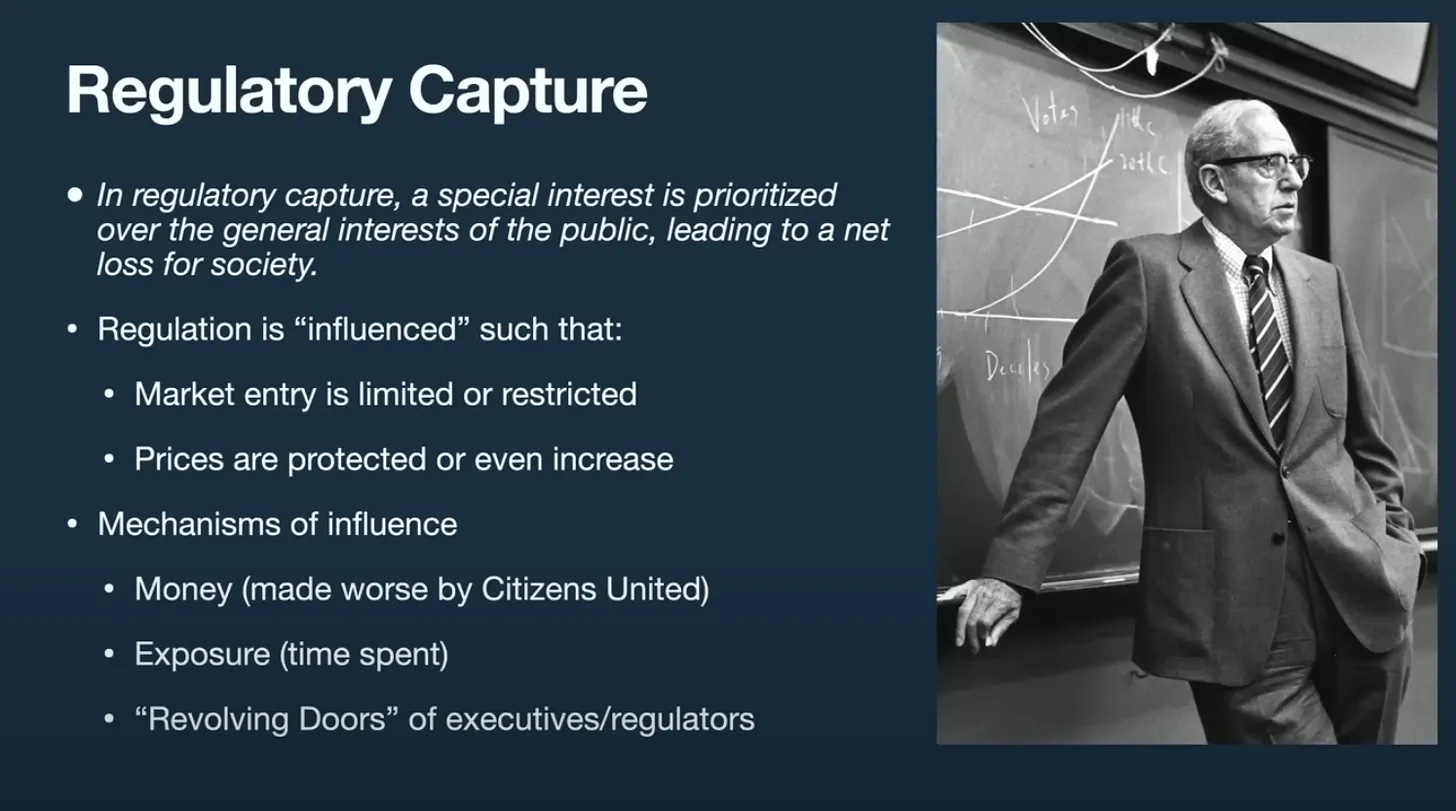

This is next to impossible currently due to multiple hurdles put forth by the regulatory bodies ( why ?)

The regulatory bodies favour large corporations via “Regulatory Capture” :- Which favours incumbents / established players of the industry

Inspiration : Bill Gurley’s talk

Here come the large financial institutions - (E.g. Banks), why is RBI shutting down multiple Fintech startups, making new regulations for the same ?

Lobbying and influencing so by :

Money they bring to the table

Access / exposure they to the policy makers

Eventually regulations / hurdles favouring them

Many of these large financial institutions are into Health Insurance as well

Making it incredibly difficult to be in the Health Insurance space : - Regulations and compliance hurdles impossible for startups to cross - Insurmountable amount of capital as a buy-in

B) Adding value to consumers’ Health outcomes

Verticals for Core value add in patient’s health cycle :

Diagnostics

Professional Health Services

Primary + Secondary Care

Tertiary Care

Treatment / Medicines

Disease Management / Rehabilitation

Fitness / Wellness

Current Large scale disruptors in Indian HealthCare

The unit economics in Health Care startups is very difficult to crack, especially when it comes to CAC and LTV :

1. High Customer Acquisition Costs (CAC)

Low Trust and Awareness: Consumers are skeptical about the quality of new, especially digital, healthcare providers → significant spending on brand building

Fragmented Market: Split in rural and urban sectors, reaching customers across regions and income levels requires highly targeted campaigns, which are costly and difficult to scale efficiently.

2. Low Lifetime Value (LTV)

Irregular Engagement: Unlike other sectors, healthcare consumption is often episodic rather than continuous → only when there is acute need → reduces LTV.

Price Sensitivity: Healthcare expenses are often considered discretionary unless there is an urgent need → constraining revenue per user.

Customer Retention: Market is heavily dependent on trust, people are skeptical and often go for offline channels or for second opinions → eroding the LTV.

Low Willingness for preventive care: Inclination to have preventive care via regular checkups or health management programs isn’t common → limiting recurring revenue.

How are these issues affecting startups ? What am I talking about :

Pharmeasy and 1mg can been seen to have high Revenue to Burn ratio as

CAC is high → Mostly digital acquisition (with broad targeting)

Low LTV → Most products (e-pharmacy) and services are low margin and don’t contribute enough to bottom-line. Hence PharmEasy has expanded to other verticals as well to capture value at various stages.

Why are Cult.fit and Pristyn in a better position (at least in #s) ?

CAC still remains an issue for both :

For Cult:

High Churn due to inherent nature of the fitness industry, needs offline acquisition → retention & NPS of power users plays a key role.

For Pristyn:

Critical care industry → heavy reliance on trust / brand building (since products are non-standard / patient specific) → only solution is referrals / word of mouth through via NPS / customer satisfaction.

Difficult to target segment of population who would be looking for surgeries

Offline / Doctor incentives not aligned

But how is LTV solved for ?

For Cult:

Engagement for retained customers is high

Pricing is at par with the market

For Pristyn:

Price Sensitivity exists but the average ticket size is inherently high for surgeries

Not dependent on repeats

Willingness to pay is high → as these are tertiary care needs

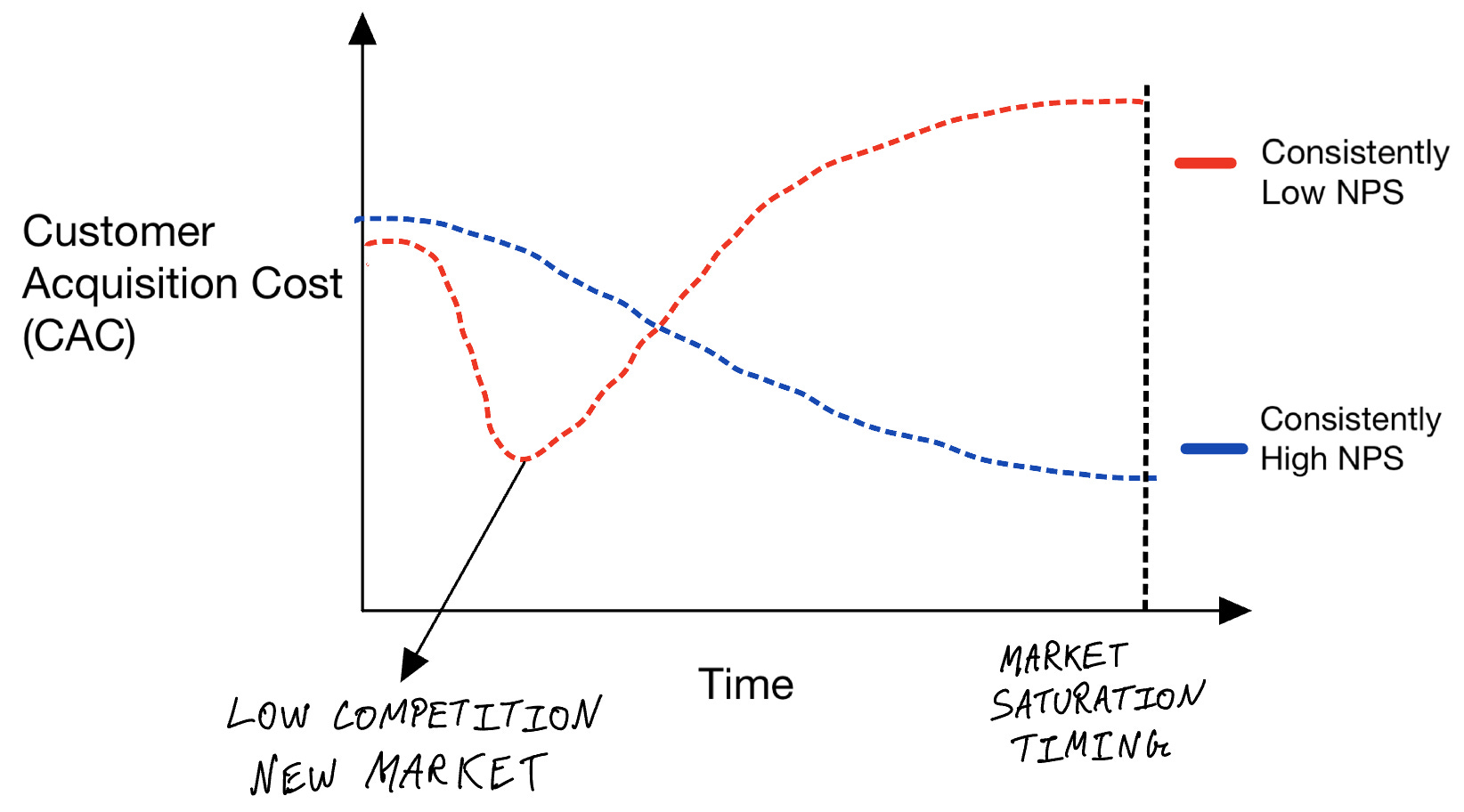

Ideal Health Care startup would look like :

A) Has figured out solving for trust & targeting customers

Should have consistently high NPS

CAC should have an improving trend = negative slope

High CAC leads to bad Unit Economics for the business → leading to issues with profitability once significant scale is attained.

B) Prove high LTV exists

LTV = Average purchase size x Number of purchases x Retention period

Hence the levers are:

Purchase Size

Number of Purchases

Retention Period

General attributes of LTV levers for various verticals:

There are still a few open spaces in the HealthCare industry for startups to capture.

If a company can capitalise on the high attribute corresponding to their segment’s levers and along with it work on changing either of the other two levers in their favour, generally leads to solving for the LTV issue for healthcare businesses.

Thank for sharing, would like to know more about regulation capture in fintech, sector wide...