Is RBI killing Fintech Innovation ?

Why P2P lending is the current target ?

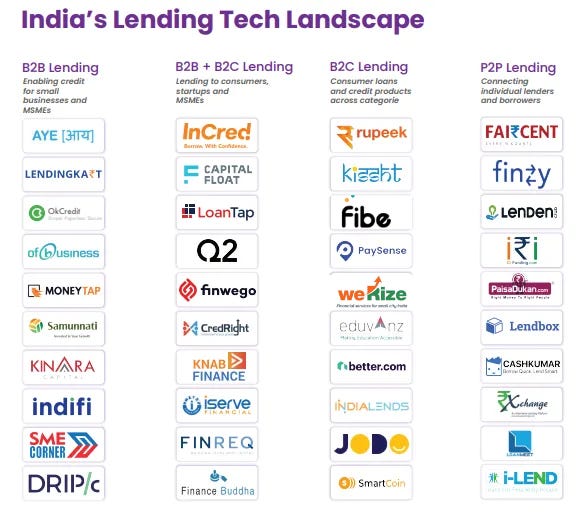

Regulatory challenges are one of the most significant hurdles for FinTech startups, as they must navigate a fragmented framework, strict guidelines and licensing requirements. Many you see in this picture below (from 2020) haven’t survived, here is the explanation:

How the ruckus started and why did RBI come in ?

What the RBI strictly doesn’t want :

Long term unregulated credit eventually leads to a debt crisis, due to:

Improper Risk assessment → High Defaults

High Interest Rates → Debt Traps

No visibility to check either of the above points (unregulated)

Culprits have been two over-exploited models :

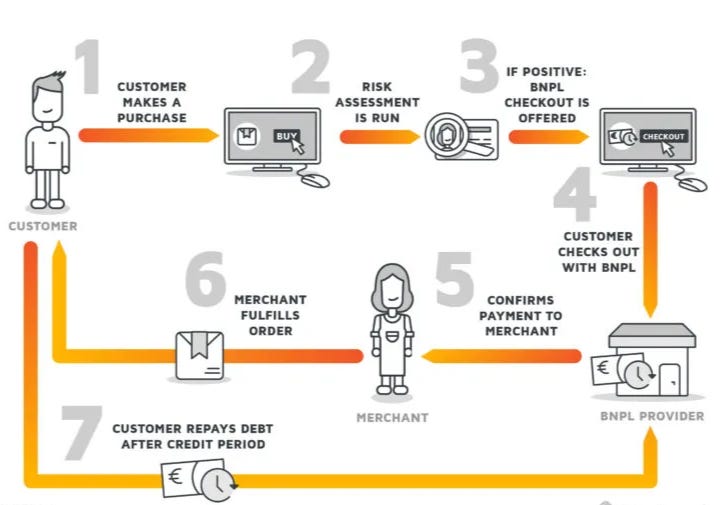

A. Buy Now Pay Layer (BNPL)

E.g. Allows customers to break large payments into zero interest EMIs

Structured as non-credit transactions = no credit reporting = No visibility to RBI

Hidden fees and high penalties for late payments = High Interest Rates

No risk assessment → Microfinance crisis

RBI's Actions on BNPL

✔ Stricter digital lending norms (only RBI-regulated entities can lend).

✔ Crackdown on unregulated fintechs (KYC & credit assessment enforcement).

✔ Push for BNPL transactions to be reported to credit bureaus.

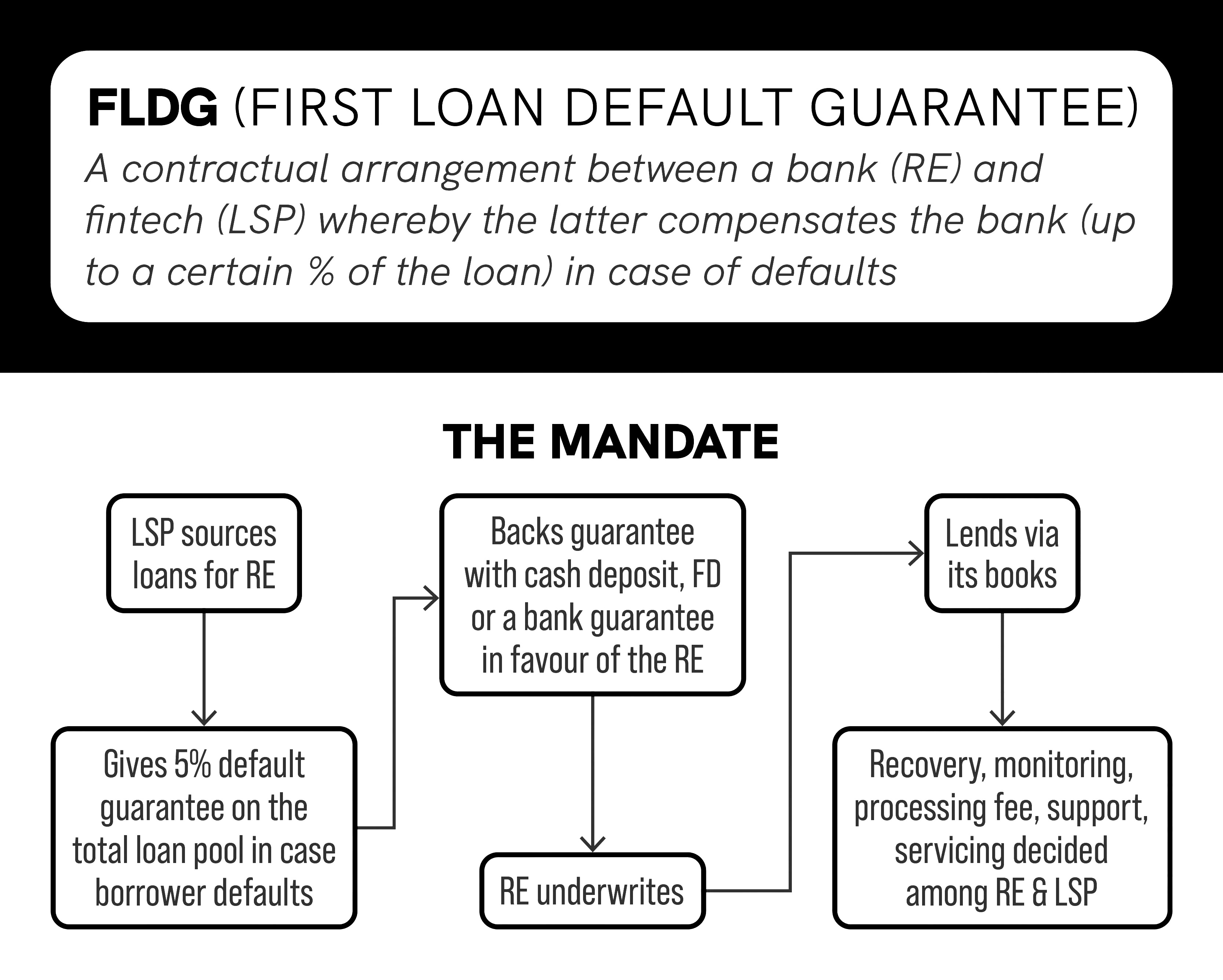

B. First Loss Default Guarantee (FLDG)

Means: If a customer defaults → the Lender (bank / nbfc) will be made whole by the Fintech as per the guarantee

Unregulated fintech firms give credit risk guarantees to NBFCs & Banks

Since Bank & NBFCs are made whole they do not report the defaults = No visibility to RBI

Incentives for NBFCs for aggressive lending → over-borrowing → Debt traps

Unchecked this would result in millions being in debt traps → systemic financial instability

RBI’s Action on FLDG

✔ In September 2022, RBI banned FLDG for digital lenders as part of its digital lending guidelines to prevent unregulated credit risk sharing.

✔ In June 2023, RBI allowed a restricted FLDG model—capped at 5% of the loan portfolio, provided fintechs are regulated and disclose guarantees properly.

✔ Co-lending introduced with 80:20 ratio for NBFCs / banks : Fintech

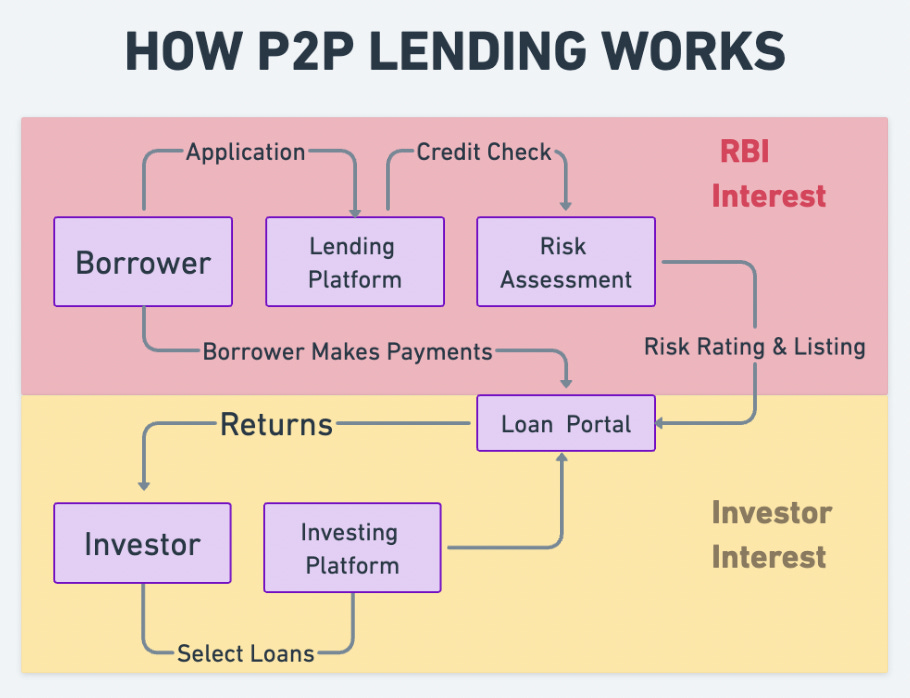

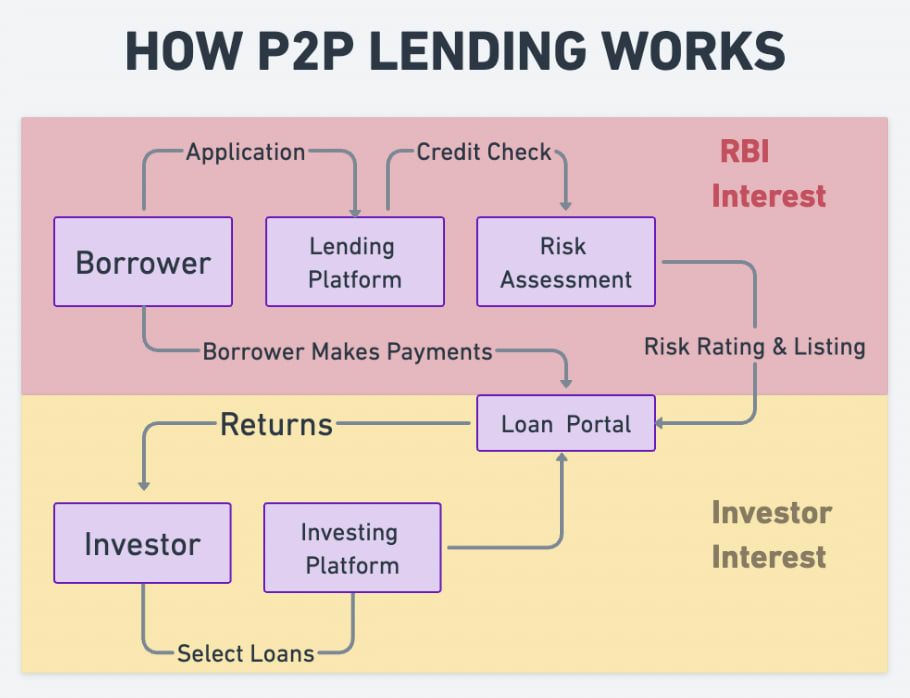

The whole P2P Lending Debacle, why is it happening ?

1. Lack of a Unified Regulatory Framework

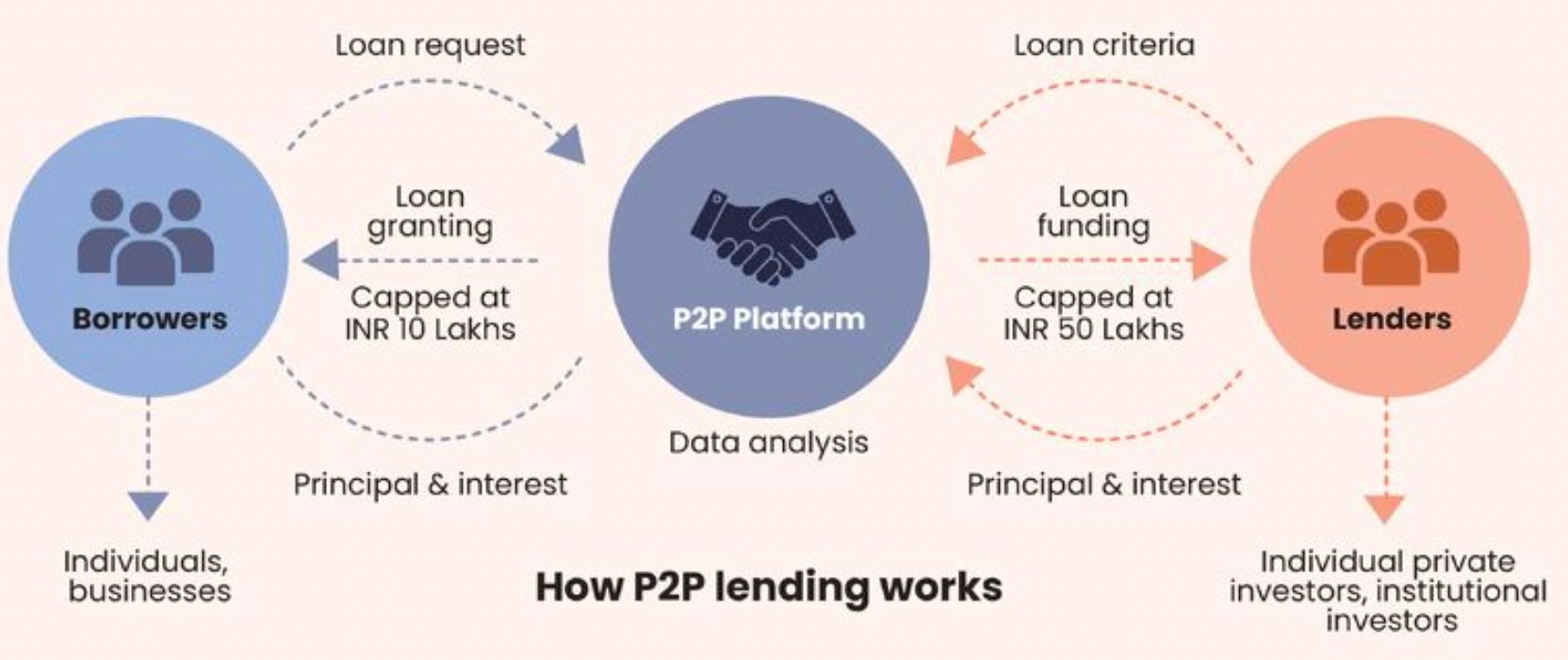

P2P lending platforms are regulated (RBI)

P2P lending platforms are regulated by the Reserve Bank of India (RBI).

The RBI has been tightening the regulatory framework for these platforms over the years.

In Aug 2024, the RBI flagged certain violations and revised P2P lending norms and halted operations of multiple platforms.

How investors leverage P2P lending platforms

Offer investors the potential for higher returns compared to bank fixed deposits, though returns are not guaranteed.

The platform identifies, vets and distributes investor funds among multiple borrowers, reducing the risk for investors.

Investors have been investing in P2P lending platforms as vehicles for extending private debt.

2. Interest rates and risk - unregulated

Similar lessons as from BNPL & FLDG

Both the borrower and lender were not visible to RBI and SEBI came in as well - as it is investing

High Interest rates or loans to no creditworthy borrowers → Debt traps

Key Provisions of RBI Guidelines:

✔ All loan disbursements and repayments must flow directly between borrowers and regulated entities (banks or NBFCs).

✔ Lending Service Providers (LSPs) must disclose all fees and charges upfront.

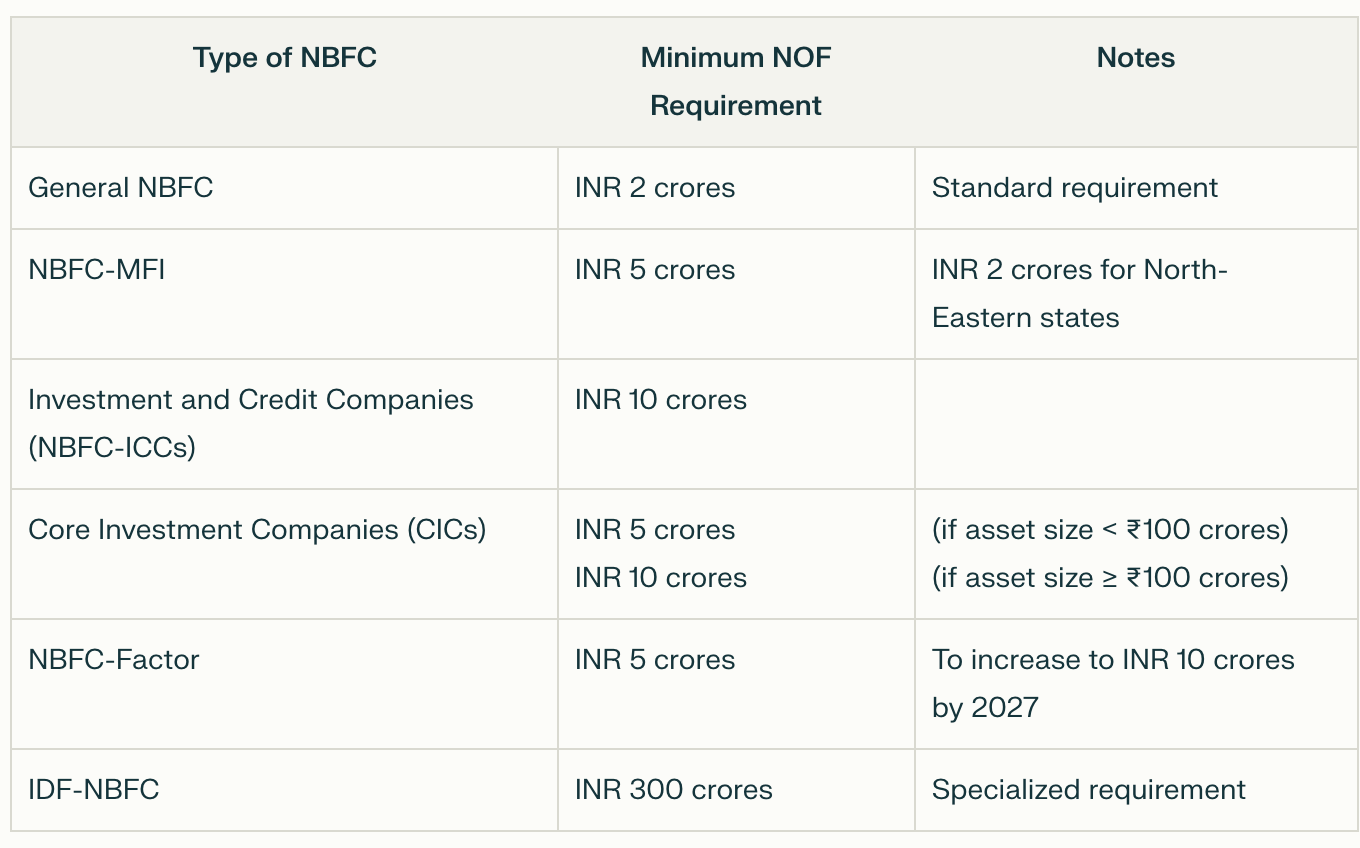

3. Licensing and Capital

Given P2P startups need to have NBFC license which is a complex and capital-intensive process.

NBFC Licensing: Obtaining an NBFC license requires a minimum net owned fund (NOF) of ₹5-10 crore, which is a significant barrier for smaller startups.

P2P Lending: The RBI mandates that P2P lending platforms maintain a minimum capital of ₹2 crore and adhere to strict operational guidelines.

With NPAs at ₹1,163 crore, that’s over 17% of the total lending in the sector. That’s not just bad, it’s potentially catastrophic.

Impact on Startups

P2P lending platform must adhere to new RBI guidelines. This increases operational complexity and costs.

Many platforms have had to renegotiate partnerships with banks and NBFCs, while others have exited the market due to the inability to comply.

Capital need → forced to operate as intermediaries → limited revenue potential and increases dependency on NBFCs.

P2P is an imported Concept. In India, P2P does not happen this way. Rather people give money in cash to friends, family, neighbours etc. That's P2P. Where there is no one in between P & P. So P2P.

My Fintech is a SaaS+ Innovative Embedded Finance. But some call it P2P, when they don't get new element of New Category of embedded finance I m operating into.