India's logistics landscape has transformed significantly over the decades, adapting to evolving market needs, technological advancements, and changing consumer expectations. Each version of logistics—1.0, 2.0, 3.0, and now the emerging 4.0.

Emerged to cater to the growing GDP - B2B commerce sector in the late 1990s and early 2000s.

Focused primarily on inter-city connectivity to facilitate mid-mile logistics.

Built a backbone of infrastructure to connect businesses across cities.

Major Players:

Safexpress: A pioneer in supply chain solutions offering pan-India coverage.

Gati: Known for reliable inter-city freight services and express distribution.

Others: Blue Dart, DTDC, and regional logistics players.

Impact:

Streamlined mid-mile logistics by improving road and rail connectivity.

Created networks that supported manufacturing hubs, wholesalers, and distributors.

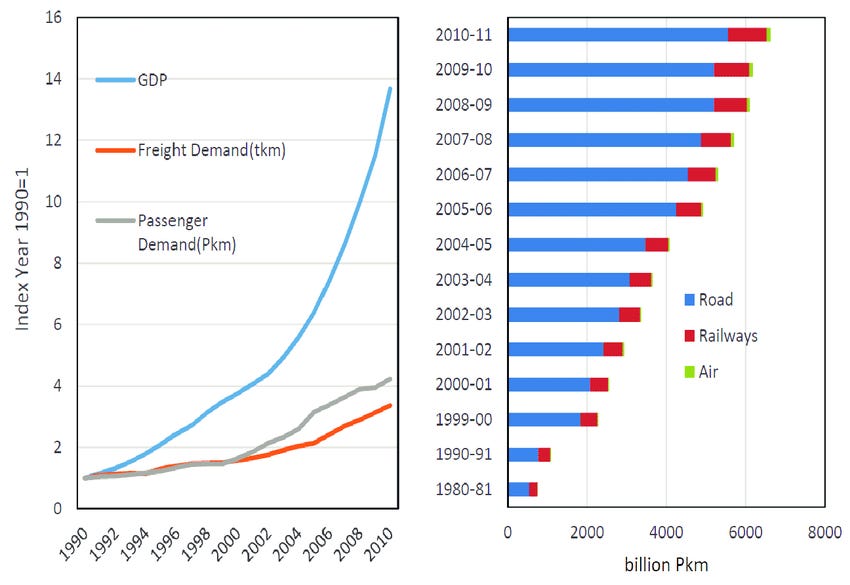

Growth in Inter-City Logistics (1995-2010)

Inter-city logistics demand skyrocketed in sync with the GDP growth and industrial expansion.

Logistics 2.0: E-commerce Boom & Reach Expansion

Key Features:

With the advent of e-commerce giants like Flipkart, Amazon, and Snapdeal, logistics providers had to adapt.

Emphasis shifted to solving for reach, covering even remote pin codes at affordable prices.

Here 3PL (Third part logistics) players focused on first-mile and mid-mile logistics, with last-mile delivery handled by e-commerce companies themselves.

Major Players:

Delhivery: Revolutionized e-commerce logistics with technology-driven solutions.

XpressBees: Tech-based logistic and supply chain solutions

Ecom Express: Built efficient first and mid-mile networks.

Others: Rivigo and Blackbuck faced challenges during COVID-19 but contributed to efficient trucking solutions.

Impact:

Expanded logistics networks to rural areas, bringing e-commerce to the masses.

Catalyzed the growth of SME participation in e-commerce.

Graph: E-commerce Growth vs Logistics Coverage (2010-2020)

Illustrating how logistics networks expanded alongside the e-commerce boom.

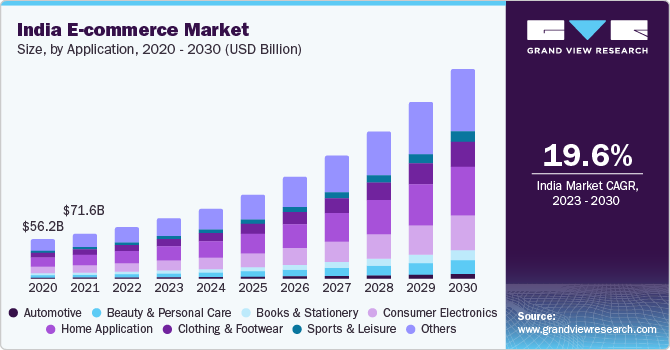

Market size of e-commerce industry across India from 2014 to 2024, with forecasts until 2030

Logistics 3.0: Empowering MSMEs & D2C Brands

Key Features:

Driven by the rise of D2C brands and MSMEs, logistics providers pivoted to full-stack solutions.

Services extended from first-mile pickup to warehousing, mid-mile transportation, and last-mile delivery.

Enabled small businesses to access enterprise-grade logistics.

Major Players:

Shiprocket: Empowering D2C brands with robust logistics solutions.

Shadowfax: Leveraging gig workers for hyperlocal delivery systems (first & last mile)

Porter: Focused on intra-city logistics for small businesses.

LetsTransport: Simplified trucking for MSMEs and enterprises.

Impact:

Democratized logistics by making high-quality services accessible to businesses of all sizes.

Supported the boom of India’s D2C economy, especially post-pandemic.

Chart: MSME and D2C Contribution to Logistics Demand (2015-2023)

Growth in logistics demand attributed to MSMEs and D2C brands.

Multiple large D2C brands have grown from 2015 onwards.

Propelled by the rise of quick-commerce (Q-commerce), emphasizing <4-hour delivery. Logistics 4.0 is transforming the landscape with hyper-local delivery networks and an emphasis on speed. Companies are leveraging micro-warehousing, dark stores, and predictive analytics to ensure rapid order fulfillment.

Logistics companies must prioritize speed of delivery over other factors.

Partnerships between Q-commerce players and 3PL providers are crucial for scaling.

Why the buzz ?

There is fundamental shift in consumer behaviour / expectations - which have risen drastically, coupled with increase in disposable income.

Quick commerce platforms are becoming the default search options.

Whatever products sell on Amazon can be brought to Q-comm channels basis central or localised dark store model.

Now the urban consumer wants these products with higher expectations - to get it quickly (not wait 2-3 days) and sitting at home and not having to visit the store (convenience) that gets enabled through Q-comm.

Q-comm will not only eat the Kirana market but also e-commerce

Why do you think Amz and Flipkart are hustling to get into q-comm.

Dunzo: An early mover in quick-commerce but hampered by an unsustainable business model. even Shadowfax is trying to provide dedicated fleet for quick-commerce operations.

Blitz, Zippee, Pico, Blowhorn: Building on-demand 3PL delivery solutions to cater to Q-commerce needs.

Early Challenges

High capital requirements for infrastructure.

Complexities in demand forecasting - Density of orders

Future Trends:

Established brands will integrate quicker deliveries via their own websites and retail outlets.

The movement of established brands will also be to their own channels (website & retail) to improve their margins - which currently take a hit on both E-comm (Amz, Fkt etc.) & Q-comm (Blinkit, Zepto etc.)

Growing order density will further push towards better unit economics for the Quick commerce platforms, pricing will play a crucial role

Validations:

A. Graph: Q-Commerce Market Growth Projection (2023-2030)

Forecasted rapid growth in Q-commerce and the logistics industry’s adaptation to speed-focused models.

B. Large D2C Brands have 20-30% order volumes and already spend a large share on logistics and deliveries, same can be channels to 3PL players enabling quick commerce.

There is enough demand and supply for products in India - with trust on online channels increasing (Amazon, Flipkart etc.) only indicates the shift of buying behaviour of consumers to E-commerce.

With increasing expectations of the customer, clubbed with increasing disposable income leads to inclination towards convenience, even with weird memes:

This boosts the prospects of quick-commerce for the products they can work out the unit economics for.

Hence whenever their is an eventual thesis of :

High growth in a new segment / industry

Demand and Supply consistently rising.

All this works in favour of 3PL :

More geographies being opened by Q-comm platforms

As brands expand to selling on quick commerce and their own website.

Eventually E-comm platforms (Amz, Fkt, Nykaa, Purplle etc.) wanting to start their own q-commerce

One should bet on infrastructure which in case of quick commerce is the 3PL Q-comm delivery companies

All this will be enabled by 3PL Q-comm companies.

“In a gold-rush sell shovels”

Possible models for 3PL quick commerce:

Dedicated delivery agents

Basically providing a fleet of riders (on per hour basis) to a particular platform or brand to fulfil the orders asap.

Issues with Unit economics due to low utilisation

Due to low frequency and density of orders

Leading to significant idle time for drivers

Although this can be a good way to test / experiment out feasibility of Q-comm deliveries

Managed Dark store model

Managing dark store and delivery fleet for a platform, brand or incumbent

Works more like a managed franchise play

Profitable from the since revenue is made basis B2B contracts

Limited scale - dependent platforms one works with.

Multi-tentant dark store

Aggregating inventory of various brands under one roof - with a promise to make deliveries in the quick commerce periods (< 4hrs)

Technically the most profitable approach for 3PL

Difficult unit economics currently - might improve with scale as density & frequency of orders increases gradually

Currently can be operationally profitable only in mature q-comm geographies

High capital requirements

Network Based approach

Q-comm deliveries on SDD network (same day delivery)

Starting with longer period deliveries (e.g. delivery within 12-24 hrs) = SDD

Utilising the same network to map q-comm deliveries in real-time

Operational nightmare - can be solved with tech (think pooling for shared rides - OLA, Uber)

Most asset-light way of execution

Eventually will morph into Multi-tenant dark store model

Key Takeaways Across the Phases

Conclusion

The evolution of logistics in India underscores the sector's ability to adapt to changing market needs. From inter-city freight solutions in the Logistics 1.0 era to the current speed-driven Q-commerce logistics in the emerging 4.0 phase, the industry has consistently embraced innovation to drive growth.

As long as there is commerce happening there will be constant evolution of logistics to facilitate the same.

In the current phase as we move forward, the focus on speed, sustainability, and technology will shape the next phase of logistics in India - the customer behaviour change due to Quick Commerce is the key driver.